Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Coldwell Banker

2024 Real Estate Market Report

North Lake Tahoe -Truckee

Residential Properties – Single Family Homes and Condominiums

Activity for the calendar year 2024

Residential Sales Summary 2024

Total Residential Sales:

Despite demonstrable headwinds, including inflation, interest rates, insurance costs, and a cooling national real estate market, the Lake Tahoe Truckee market continues to show remarkable stability. While the number of transactions in 2023 and 2024 are the 2 lowest years of the last ten, pricing has either increased or held steady in most market segments over the last year.

For 2024, the total number of residential transactions increased by 2% compared to 2023 but still ended up 25% below the 5 year average and 26% below the 10 year average.

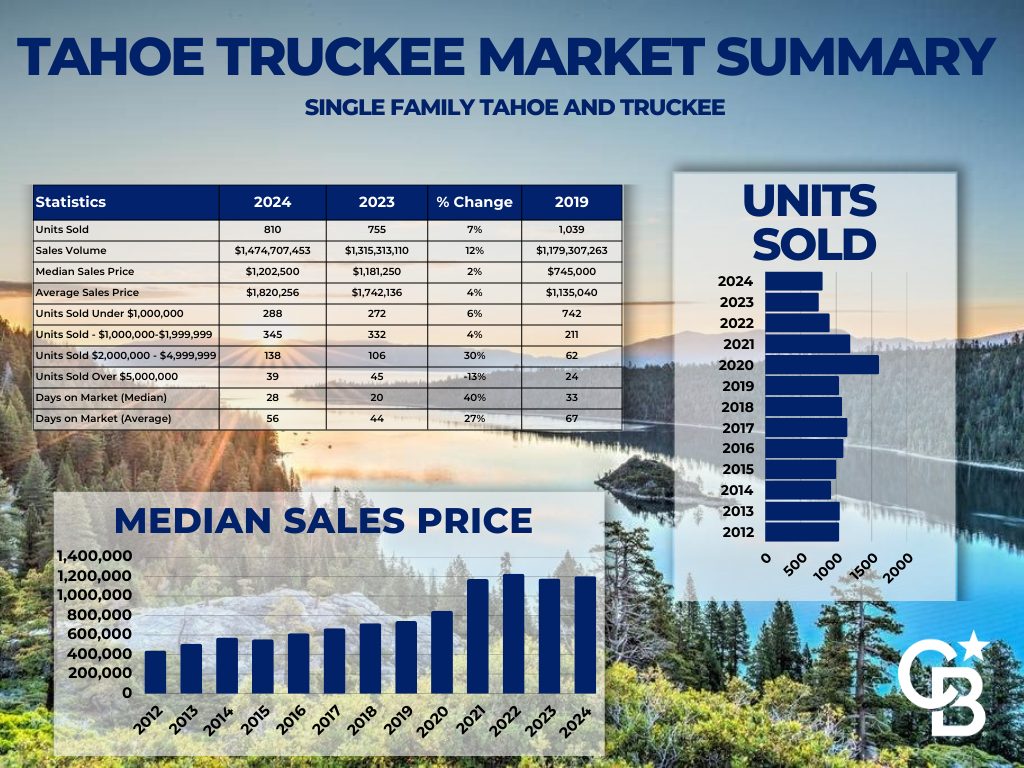

Median and Average Sales Prices: The median price of a residential sale increased by 6% (from $1.06 million in 2023 to $1.125m in 2024) while the average sales price increased by 5.4% (from $1.544 million to $1.628 million).

For single family homes the median was up 4% (from $1.181m to $1.203m) and the average price was up 4% ($1.742m to $1.82m).

For condos the median price was down 2% (from $726k to $710k) and the average was down 1% (from $998k to $983k).

Prices are at a very healthy premium from where they stood in 2019 (before COVID). For single family homes the median sales price is up 61% compared to 2019 (from $745k to $1.203m) and the average sales price is up 60% (from $1.135m to $1.82m).

For condos the median sales price is up 65% compared to 2019 (from $430k to $710k) and the average sales price is up 77% (from $555k to $983k).

Active Residential Inventory:

Active Listings: Supply increased in 2024 relative to 2023, but the total number of homes that came on the market was only 90% of the 5 year average and 82% of the 10 year average. Inventory was slightly higher throughout the year compared to 2023 but remains well below pre-covid levels.

We are in the heart of winter when inventory hits annual lows. There are 260 residences currently on the market. Last year, at this time, there were about 230 residences actively for sale, but in 2019 the number was closer to 400.

Current Pending Sales: The number of pending sales is at 71 (up from 55 last year at this time).

Current inventory represents a little over 4.2 months of supply relative to December activity. Historically any number below 5 months of supply is considered a seller’s market. But, overall, this is a very balanced market.

Sales Under $500,000: In 2024, there were 46 residential sales under $500k, representing 4% of total sales. In 2023, 6% of sales were in this range.

Mid-Range Market Sales $500,000 to $999,999: For the year, 409 residences sold between $500,000 and $999,999, representing 39% of total sales. In 2023, 40% of sales were in this price range.

High End Home Sales $1,000,000 to $1,999,999: 398 residences sold between $1m – $2m, representing 38% of total sales. In 2023, 37% of total sales were in this range as well.

Luxury Home Sales Over $2 Million: 201 residences sold over $2 million in 2024, representing 19% of total sales. This includes 39 sales over $5 million, of which 11 were over $10 million and 1 over $20 million. In 2023, 180 residences sold over $2 million, representing 17% of sales. This included 46 sales over $5 million, of which 7 were over $10 million.

What’s Going On Looking Forward?

There’s optimism in the local real estate market because of solid activity early in the year, especially in the luxury market (residences over $2 million). A strong stock market and a new administration that is “real estate friendly” are likely to help us in the year ahead. However, I’m hesitant to predict that market activity will change significantly in 2025. The continued increase in cost for insurance and higher interest rates will certainly be headwinds.

If the market does change significantly, it will likely come from something not currently on our radar.

Low inventory will continue to be a reality in the market. We do not expect inventory to approach levels we saw in the pre-COVID benchmark years.

Multiple offers on properties have become uncommon and bidding wars (5+ offers) have almost gone away. However, properly priced homes will still sell quickly. Reduction of asking prices is common but mostly occurs on homes that weren’t priced properly to begin with.

Sellers, keep in mind, this is still a much better time to be a seller than it was in 2019 (which seemed like a very healthy market at the time!). You can expect a similar time on market, but much higher sales prices!

Buyers, keep in mind, this is the most balanced market we have seen in the last 4 years. You now have the following things working in your favor:

- The ability to negotiate price is back!

- The ability to inspect a property and have normal contingencies is back!

- The ability to negotiate repairs is back!

- Yes, interest rates are higher than we got used to but are in the “normal” range historically speaking. We do not expect significant changes in interest rates in the foreseeable future. If/when they do start to drop, it will likely cause an increase in demand and increased prices. You are better off to buy now, in a relatively balanced market, and refinance when rates drop.

Contact Your Coldwell Banker Agent Today to Find Out More about the Opportunities Available in the North Lake Tahoe-Truckee Market.

Note: Data on this page is based on information from the Tahoe Sierra Board of Realtors, MLS. Due to MLS reporting methods and allowable reporting policy, this data is only informational and may not be completely accurate. Therefore, Coldwell Banker Realty does not guarantee the data’s accuracy. Data maintained by the MLS may not reflect all real estate activity in the market. CA-BRE License # 01908304